Translation option:

The organization of food supply chains (FSCs) is strongly affected by the level of economic development and factors such as urbanization and globalization. COVID-19 will thus have different impacts on FSCs in poor vs. in rich countries. Tom Reardon, Marc Bellemare and David Zilberman identify these structural differences and draw out the implications of widespread lockdowns and possible policy responses.—Johan Swinnen, series co-editor and IFPRI Director General.

COVID-19 is spreading through the developing world. Many low- and middle-income countries are now reporting growing numbers of cases and imposing rigorous lockdown regulations in response, which impact all aspects of the economy. How will COVID-19 affect food-supply chains (FSCs) in developing countries?

The evidence suggests that the impacts will be felt widely, but unevenly. Farm operations may be spared the worst, while small and medium-sized enterprises (SMEs) in urban areas will face significant problems. Governments will have to develop policies to respond to these varied impacts to avoid supply chain disruptions, higher food prices, and severe economic fallout for millions of employees.

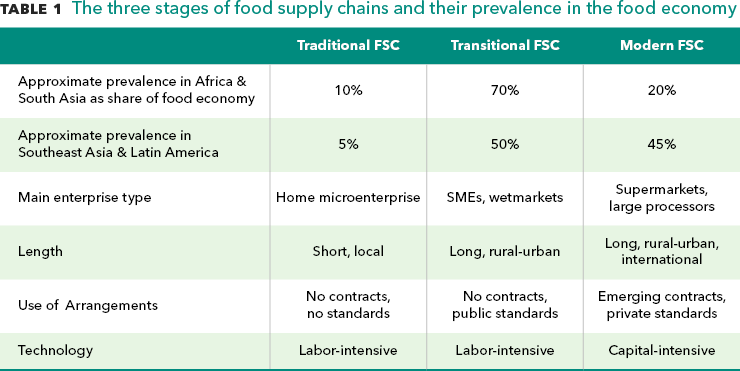

For context, here is what the literature tells us about FSCs in developing countries (see also Table 1 below):

- Most urban and rural consumers now depend on markets, in contrast to 30-40 years ago when a large share of rural populations lived “off the grid” in subsistence agriculture. Consumers purchase 80% of all food consumed in Africa and Asia, and thus FSCs provide 80% of all food consumed (Reardon et al. 2019).

- Modern FSCs (dominated by large processing firms and supermarkets, capital-intensive, with relatively low labor intensity of operations) constitute roughly 30%-50% of the food systems in China, Latin America, and Southeast Asia, and 20% of the food systems in Africa and South Asia.

- Transitional FSCs (stretching from rural to urban areas, fragmented and dominated by thousands of labor-intensive SMEs) dominate food systems, with 50%-80% of the food economies of developing Asia and Africa.SMEs in transitional FSCs in developing countries tend to be found in clusters such as dense sets of food processing SMEs, scores of meal vendors at truck stops, and dense masses of wholesalers and retailers in public wholesale markets and wet markets. Each of these clusters could have numerous SMEs. In these venues, large numbers of clients gather in dense crowds.

IFPRI. Source: Authors’ note

What might happen to food supply chains

Here are seven hypotheses, based on what we know so far, about the likely effects of COVID-19 on FSCs in developing regions:

- Direct impacts will overwhelmingly be felt post-farm. Namely, the “midstream” (e.g., wholesale, logistics, and processing), and “downstream,” in food-service enterprises.

- The impacts are likely to be largest in dense urban and rural peri-urban areas. Given the properties of the novel coronavirus, which is transmitted most easily via human contact, greater population densities tend to facilitate its spread.

- Effects will be strongest in the downstream segments of retail and food service. These downstream firms are mostly informal-sector SMEs, and are thus labor-intensive with high densities of workers in small spaces. They have little control over the hygiene practices of their product suppliers or customer habits.

- Retail and food service firms in modern FSCs face fewer problems. They are far less vulnerable to mandatory business closures, and also face a lower risk of clients and employees contracting the disease. The least affected are likely to be supermarket chains. Their stores can enforce the flow of entering customers and social distancing measures. Supermarkets and fast-food chains also have more control over the food safety and hygienic practices of their FSCs, as they typically vertically coordinate with contracts and private standards (Swinnen 2007).

- Direct impacts on farm population and farm production will be much smaller than on the FSC downstream and midstream. This is because most small farmers in developing countries rely on family labor. The farm sector, however, will be affected indirectly by COVID-19 through the disruption of input supply chains, and of consumer demand due to lost income and other economic impacts of the pandemic.

- COVID-19 is likely to increase food prices, both as a cause and consequence of food shortages. Restrictions on FSC logistics will increase transaction costs and thus consumer prices. Speculative hoarding may occur and trigger price increases. Higher food prices are, in turn, likely to signal impending shortages. These effects can compound each other in a vicious cycle likely to cause social unrest (Bellemare, 2015).

- COVID-19 responses will create economic hardship. Enforcing social distancing and limits on internal and external logistics in FSCs, will transform health risk problems into income and employment risks, and political risks.

Implications, strategies, policies

Clearly, the segments of FSCs in the developing world most vulnerable to COVID-19 impacts are the midstream and downstream segments. This will present significant challenges for the people working in them and likely lead to broader economic and operational changes going forward.

As most of these FSCs are in the “transitional” stage, they are composed mostly of informal sector SMEs, with employees lacking formal registration and safety nets such as unemployment insurance.

In the short term, millions of these businesses will face lower foot traffic, lower incomes, and substantial unemployment.

In the medium term, COVID-19 impacts on these segments may be like past episodes of avian flu in Southeast Asia in the 2000s, which induced rapid concentration, leading to the rise of large processing firms and supermarkets.

How should governments respond to minimize supply chain disruptions and fallout from lockdowns and other restrictions? The general strategy must be two-pronged: Implement robust public health measures to slow the spread of disease; and address food security impacts, particularly the potentially enormous effects on income and employment.

This strategy presents significant challenges for developing countries. Addressing the FSC issues will require three complementary policy paths: In the short run, implement new, broad safety nets for SMEs and workers in the midstream and downstream segments of FSCs; for example, governments could use cash-for-work schemes to employ workers to distribute emergency food rations, upgrade sanitation in wholesale markets and wet markets, and maintain essential operations in their own enterprises so that the latter are there when the crisis passes. In the short and medium term, monitor and regulate wholesale markets, retail wet markets, and processing clusters more strictly, and redesign their sites for improved health practices. Finally, make long-term investments to help SMEs change hygiene practices and better site design that will help them remain competitive.

Thomas Reardon is a Professor in the Department of Agricultural, Food, and Resource Economics at Michigan State University; Marc F. Bellemare is a Professor in the Department of Applied Economics at the University of Minnesota; David Zilberman is a Professor in the Agricultural and Resource Economics Department at the University of California, Berkeley. The analysis and opinions expressed in this piece are solely those of the authors.